FACTORS TO CONSIDER WHILE BUYING A LIFE INSURANCE TERM PLAN

How to buy a Term Life Insurance Plan?

In this article, we would be discussing and understanding factors to consider while buying a term life insurance plan.

Why you should buy Life Insurance?

Buying life insurance in today’s time is important as it helps to strengthen an individual’s ability to mitigate risk of dying early.

When you do not have a life insurance, then your loved ones are more vulnerable to financial uncertainties if something unfortunate to you. This situation can further aggravate especially if you are the primary bread winner of the family.

Death of the livelihood earner of the family leaves them financially and emotionally insecure. But having a life insurance plan helps them in handling future uncertainties by providing them financial assistance in your absence.

| LIFE INSURANCE OFFERS FOLLOWING BENEFITS: |

| Ø Life insurance plans provide a high life risk cover to protect your loved ones against unforeseen situations in life. |

| Ø Life insurance ensures that the insured’s family receives regular income post the demise of the breadwinner of the family. This income substitutes for the loss of income occurred to the family due to the policyholder’s demise. |

| Ø Life insurance offers tax benefits which is eligible for deductions upto Rs 1.5 lacs per annum under Section 80C of the Income Tax Act. The amount receives by the beneficiary post policyholder’s death is tax-free to him. |

| Ø The money invested in life insurance plans is safe and fetches good returns. The invested money is fully returned either on completion of the policy term or in case of the policyholder’s death. |

| Ø You can also buy riders or additional benefits with the life insurance policies by paying a little extra amount of premiums. These riders enhance your risk coverage by covering personal accident, critical illness benefits also. |

Therefore, it is important to buy a life insurance policy after considering all these points.It is also important to buy a good term plan by keeping your family needs in mind.

Why You should buy Term Life Insurance?

Let us first understand Term Life Insurance Product and how it is different from other life insurance products.

Term life insurance is a life insurance product where if the life assured dies during the term of the policy the claim is paid to the family and if the life assured survives the term of the policy nothing is paid to the policy holder.

Many people think that as the policy does not give anything back, so it is not a good product to buy. This is totally wrong way of thinking.

What is the primary purpose of buying Life Insurance? It is actually mitigating the risk of financial loss to the family caused due to early death of the bread winner. This objective is met by a Term Policy Plan and at the cheapest cost.

FACTORS TO CONSIDER WHILE BUYING A TERM PLAN?

A simple form of insurance is called a Term plan. A term plan is an insurance tool that offers financial protection in the form of a sum assured to your family members if something unexpected happens and at the lowest cost.

The most important factor to consider while choosing a Term Plan is the cost i.e. premium payable for the sum assured you require. Generally speaking choose the lowest premium offered for your age and sum assured.

Apart from this there can be several other decisions you need to take

- Sum Assured or Cover Amount

1) Decide on the cover amount

In order to decide on the amount of cover you need to take, you must assess and consider aspects such as:

- a) Your age and financial responsibilities

- b) Your family’s future financial requirements

- c) Your basic expenses based on your current lifestyle habits

- d) Your Financial Goals and Responsibilities

Ideally, you should opt for a plan with single premium options that offers your family the assured lump-sum amount after your death. The policy’s sum assured should be atleast 15-20 times of your current annual income.

B Determine the period of the policy

Policy Term or period of policy should be chosen taking into consideration till what age your financial responsibilities towards your family will be over. As the primary purpose of the policy is to overcome the financial loss to the family due to the breadwinner early death.

- a) Based on your age

| YOU CAN DETERMINE YOUR POLICY PERIOD BASED ON YOUR CURRENT AGE |

| Ø If the age is between 20-30 years, then a policy of 30-40 years is advisable. |

| Ø If the age is between 45-50 years, then a policy of 10 to 25 years is advisable. |

| Ø If you are looking to buy a high-cover and low premium term plan, then, it is advisable to buy the term insurance policy at an early age( because the younger and fitter you are the lower the risk you carry and hence insurance companies offer you higher life covers at very low premium rates) |

- b) Based on your retirement

If you have a retirement plan in place, then you can opt for a policy which can last till the age of your retirement. This will ensure that the cover extends throughout your working years and your family is financially stable in case of an unfortunate event related to the earning member.

- c) Based on your financial responsibilities

You can also purchase a policy based on your other financial commitments. For example, if you have taken a house loan for a period of 30 years, then it makes sense to have a term life cover of at-least 30 years which can ensure that your family is safe if any unfortunate event occurs.

3) Find suitable payout options

The premium amount of your policy is also dependent on the payout option you choose. There are simple term plans that offer a single sum of death benefit whereas there are some insurance companies as well that extends the option to receive life cover and monthly income for a higher premium.

You can choose the suitable payout option based on your priorities and your needs.

4) Choose the right insurance companies

It is very important to choose the insurance partner that best suits your needs given there are many insurance companies offering different types of plan in the market.

You should keep the following points in mind while taking the final decision:

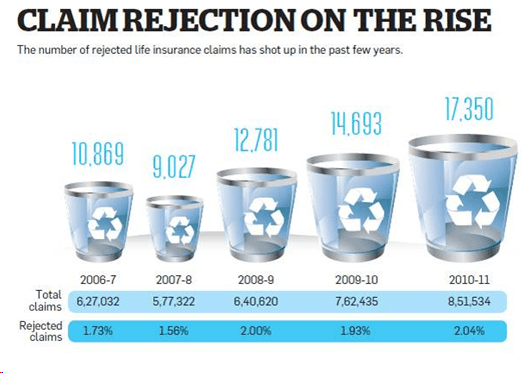

| CLAIM SETTLEMENT RATIO |

| The claim settlement ratio of an insurance company is the number of policies that are settled or the policy amount is paid back to the policyholder. It is advisable to select an insurance company that has a high claim settlement ratio. |

| SOLVENCY RATIO |

| The solvency ratio indicates the ability of an insurance company to meet its long-term dues. Selecting an insurance company with a higher solvency ratio is advisable as it indicates financial strength. |

| MARKET REPUTATION |

| It is important to find about the market reputation of the insurance company and to know more about aspects such as the number of customer complaints and grievance ratio. It is important to take insurance from a highly credible company. |

With this, we move to the next topic.

TIPS TO KEEP IN MIND WHILE BUYING A TERM INSURANCE PLAN

1) Buy a term insurance plan earlier

It is advisable to buy a term insurance plan earlier as the earlier you purchase it, the better it is.

Do not be too late in buying the policy because as time passes, your premium amount will increase depending on your age and it may get tougher to buy a policy.

2) Buy the term insurance policy only till your retirement age

It is advisable to buy the term insurance policy only till the age of your retirement. This is because not many family members will be financially dependent on you beyond your retirement age.

3) Do not buy single premium policies

It is advisable to not buy single premium policies and buy a regular premium policy while purchasing a life insurance policy. The best option which suits most of the people is the yearly premium while buying a term plan.

4) Use rider carefully

Riders are a good addition with a term insurance plan, but you should use it carefully and if you really require them. You should only add a rider to your policy when you need it and it gives you a sense of more security.

Some of the riders are:

| Accidental Death rider |

| Permanent and Partial Disability |

| Critical Illness |

5) Buy the basic version of the term insurance plan

There are various term plans in the market nowadays. The most basic one is the one which pays you a lump-sum benefit on death. It is advisable to choose the basic version of the policy as other options are designed for some very specific situations.

6) Do not hide your smoking and drinking habits

It is not advisable to hide your smoking and drinking habits while purchasing any life insurance plan. Your premium calculation happens based on this critical information and hiding this information could actually result in breaching the contract and your claim will be rejected in the end. Therefore, do not hide this information.

7) Do not hide your health information

It is advisable to not hide your health information from your insurance provider. If you have any health issues or have gone through any major surgeries, then you should communicate this information to the insurance company. One of the reasons behind rejection of claims is hiding of important facts.

Therefore, it is prudent to not hide your health information and smoking and drinking habits as it could lead to claim rejection

8) Disclose the old insurance policy

Whenever you buy any life insurance policy, it is mandatory as per the rules to disclose the old insurance policy you have already have. In most of the cases, when people buy a term plan, the fail to declare the previous policies they have bought.

Therefore, it is advisable to disclose your old insurance policies.

9) Tell your family members about the purchase of the policy.

It is advisable to tell your family members about the term plan that you have bought for your family along with the policy papers and the contact number of the insurer.

You can keep the important documents at a safe place and share the information with them.

We would like to know your views on this topic. Use the comment section below to let us know about your views and concerns.

SEO FOR THE BLOG:

url: www.planetfp.org/how-to-select-term-life-insurance

Title: How to Buy a Life Insurance Term Policy

Met description: All you wanted to know about buying a term life insurance. Factors to consider and how to select the right company and right product.

H1: FACTORS TO CONSIDER WHILE BUYING A LIFE INSURANCE TERM PLAN

H2: How to buy a Term Life Insurance Plan?

1 Comment

binance

February 16, 2024Your point of view caught my eye and was very interesting. Thanks. I have a question for you. https://www.binance.com/it/join?ref=RQUR4BEO